From our friends over at Vanguard, this article explores how parents and advisers can work together to manage intergenerational wealth transfers.

How to Build Financial Trust Across Generations

How parents and advisers can work together to manage intergenerational wealth transfers.

We’re told our time horizon shrinks as we age. This makes sense, because the closer we get to retirement, the less time we have left to accumulate wealth. And the nearer we come to having to eventually draw down on that wealth.

But retirement often throws up a whole new set of priorities. Instead of our own time horizon, we’re now thinking about our children’s time horizon; and, as they may have their own families, even their children’s time horizon.

Suddenly, the priority is not just to make your wealth last, but to preserve it for the next generation. And that’s where the real power of advice lies: its ability to transform families by building intergenerational wealth.

The Intergenerational Wealth Opportunity

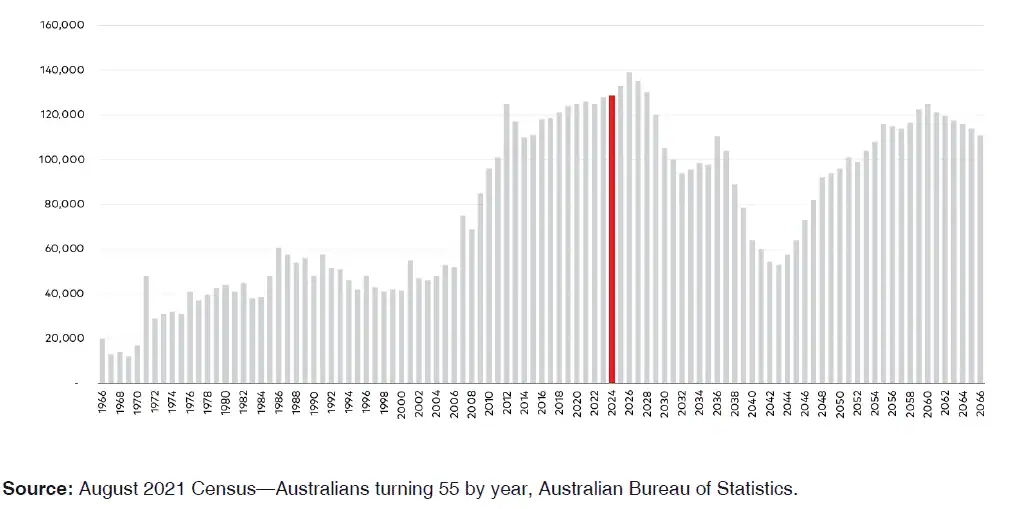

Australia is nearing the crest of a retirement wave. As the baby boomer generation looks to pass on wealth, those in receipt of it will likely need guidance.

For the emerging generation of wealth builders, what were once reasonably straightforward considerations around saving and budgeting may suddenly become more substantial.

And for both the younger and older generations, conversations around estate planning, inheritance, business succession, the family home, tax issues, and aged care can open an emotional can of worms.

Building trust with both cohorts is essential before these conversations can take place. Putting the time in now is worth it given the potential size of the opportunity.

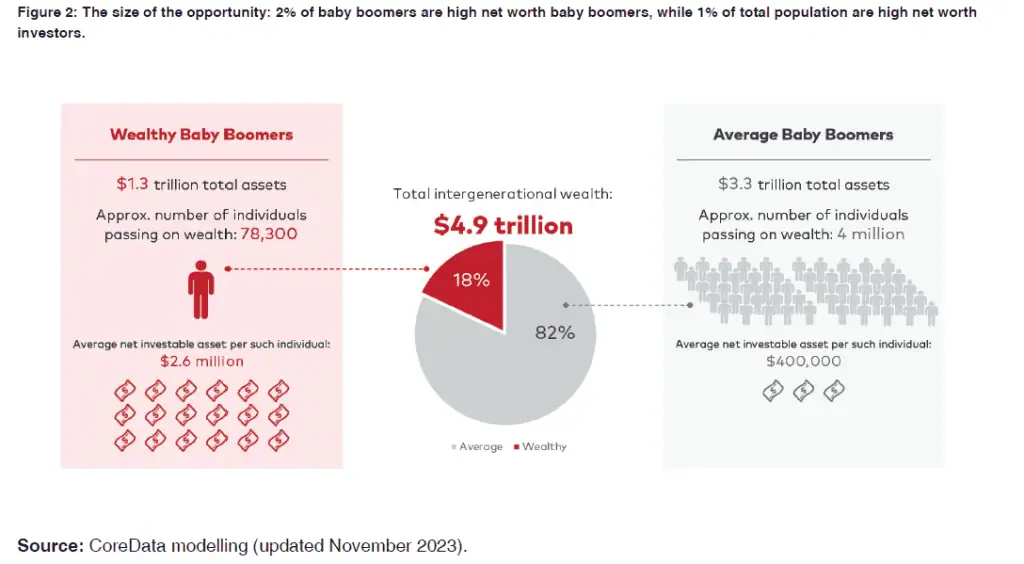

Estimating wealth in aggregate is notoriously difficult, especially when you factor in businesses, home contents, non-superannuation investments and non-financial assets. But with some modelling, we can get a reasonable idea of the wealth set to change hands.

According to CoreData Research, the baby boomer generation holds around $4.9 trillion in total assets. This wealth is held by over 4 million baby boomers, including a small group of wealthy “baby boomers” with $1.3 trillion in assets.

How this wealth gets passed on could be the biggest financial change in Australia’s history. It could also be the biggest opportunity in advice that has ever existed.

Building Trust Across Generations

We know it’s critical for advisers to reach Australians at a younger stage of life. But there’s a lot of groundwork that needs to be done before an adviser can start advising your children.

Talking to other people’s children about money is a delicate matter. Wealth transfers and inheritance planning are not regular topics of conversation at the family level. Understandably, many families find subjects such as death and the future division of wealth as unpleasant and potentially sensitive, especially when multiple heirs are involved.

Building trust across generations helps facilitate open discussions about the intended treatment of assets, as well as the ‘who’, ‘how’ and ‘when’ of transferring wealth. This requires talking to both generations, not just the older one.

Key Considerations for Advisers

Advisers may have a strong, long-standing relationship with you, but that doesn’t mean they can automatically win trust from your children.

Here are some important considerations for advisers when engaging clients across the generational divide:

Younger Clients Describe Themselves Through Their Investments: Younger generations want to invest in things they feel good about. They’re looking for advice to ensure their investments align with their values.

Building a Client Value Proposition: The value advisers provide to you doesn’t necessarily matter to your children. Advisers need to demonstrate the value and utility of their advice to your children.

Focus on the Tech Stack: Millennials and zoomers are technology-first generations. Advisers should meet them where they are when it comes to harnessing technology in their interactions and advice delivery.

Technology is no substitute for real human connection, but in the right context it can help advisers engage on a deeper level, communicate the full value of their advice, and make certain tasks quicker and easier.

When it comes to ensuring investments are sufficiently diversified, staying informed about the markets, modelling different scenarios, and monitoring investments, a significant proportion of clients prefer technology to be involved.

For trust and confidence, feeling listened to, and knowing their goals are understood, clients overwhelmingly prefer human delivery.

Conclusion

The key to successful intergenerational wealth transfers lies in building trust, open communication, and leveraging the right mix of technology and personal connection. By understanding the unique needs and preferences of both older and younger generations, advisers can help families navigate the complexities of wealth transfer and ensure a smoother transition of assets.

General Advice Warning

Vanguard is the product issuer and the Operator of Vanguard Personal Investor. Vanguard Super Pty Ltd (ABN 73 643 614 386 / AFS Licence 526270) is the trustee of Vanguard Super (ABN 27 923 449 966) and the issuer of Vanguard Super products. We have not taken your objectives, financial situation or needs into account when preparing this report so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs and the disclosure documents of any relevant Vanguard financial product before making any investment decision. Before you make any financial decision regarding a Vanguard financial product, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard’s financial products can be obtained at vanguard.com.au free of charge and include a description of who the financial product is appropriate for. You should refer to the TMD of a Vanguard financial product before making any investment decisions. You can access our IDPS Guide, Product Disclosure Statements, Prospectus and TMD at vanguard.com.au or by calling 1300 655 101. Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This report was prepared in good faith and we accept no liability for any errors or omissions.

©2024 Vanguard Investments Australia Ltd. All rights reserved.